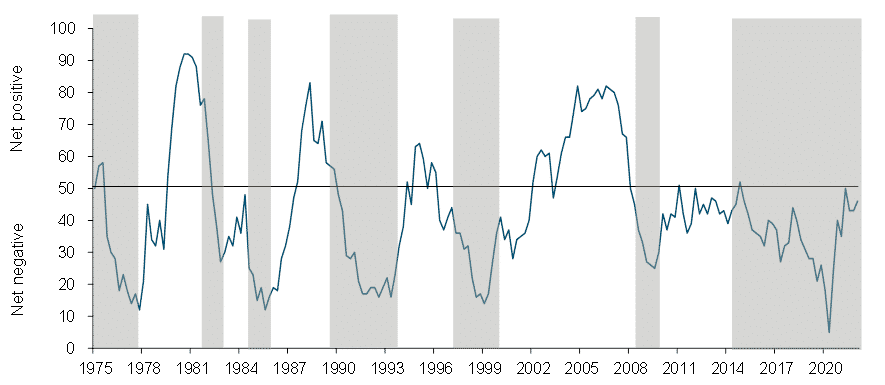

After remaining unchanged at 43 points in the fourth quarter of 2021, the RMB/BER Business Confidence Index (BCI) increased to 46 in the first quarter of 2022. Although this is just below the neutral-50 mark reached in the second half of last year, the latest reading is nonetheless encouraging in that it equals the BCI’s long-term average which, at 46, is a far cry from the five-index-point low recorded at the height of the Covid-19 pandemic in 2020.

Figure 1: RMB/BER Business Confidence Index

Source: BER, SARB (Shaded areas represent economic downswings)

The fieldwork for the first quarter survey was done from 9 to 28 February. The lion’s share of results from questionnaires were therefore submitted before Ukraine was invaded and the oil price surged past $120 per barrel. The survey covered 1 300 senior executives in the building, manufacturing, retail, wholesale, and motor trade sectors.

Details

Of the three sectors that showed an increase in confidence, new vehicle dealers saw the biggest improvement. After declining from 47 to 41 in the fourth quarter of 2021, sentiment recovered to 54 in the first quarter. Improved supply made for increased sales, but even so dealers could not fully satisfy demand as stocks remained below satisfactory levels.

Wholesale confidence edged slightly higher to 57. Sales of consumer goods weakened, while those of non-consumer goods, such as machinery and chemicals, received a boost from favourable conditions in the agricultural and mining sectors.

Also showing an improvement in the first quarter was manufacturing. Its BCI jumped from 38 to 43, owing to continued strong domestic sales and exports. Production would have increased even more were it not for ongoing supply chain bottlenecks and shortages of key inputs constraining activity.

As for the remaining two sectors making up the RMB/BER BCI, sentiment among retailers declined from 52 to 49, while confidence for building contractors edged down by five points to 25.

Retailers of non-durable goods saw the biggest deterioration in confidence as sales subsided alongside rising food price inflation, and an apparent ongoing shift by higher-income earners towards greater spending on take-outs and dining out, than on food and groceries for at-home consumption and entertainment – a trend that noticeably benefitted non-durable retailers during Covid-19 lockdown periods. Sales of durable goods such as hardware and building materials (until now driven by work-from-home additions and renovations) seemingly have peaked, while that of furniture, appliances and electronic equipment continued to perform strongly. Sales of semi-durable goods (clothing and footwear) are making a comeback of sorts.

Confidence of building contractors retreated to 25 in the first quarter. Excess supply of office, and in some instances, retail space, delays in building plan approvals, delays and even suspensions of tenders and weak demand for new standalone houses (which have become increasingly costly against existing houses which continue to see subdued price inflation), have all continued to limit the work available for main contractors. By contrast, sub-contractors (which are not included in the RMB/BCI) continued to benefit from, among other factors, office buildings being refurbished and/or converted into multi-use precincts.

Bottom line

Growing by 1.2%, the economy posted a strong rebound in the fourth quarter, shrugging off the impact from the NUMSA strike, load-shedding in November and the presence of the Omicron variant. Going by the latest RMB/BER BCI survey results, underlying demand conditions remained comparatively strong in the first quarter, especially in the case of new vehicle trade, some segments of retail, and in manufacturing. In all, the improvement in sentiment points to the economic recovery, temporarily interrupted in the third quarter of last year, having continued into 2022.

“However, the stagflationary shock brought about by Russia’s invasion of the Ukraine has now triggered a significant degree of uncertainty around global, and by implication, SA’s GDP growth prospects”, said Ettienne le Roux, chief economist at RMB. This is most unfortunate as it happens at a time when the economy seems to have been well on its way to a full recovery from the significant output losses incurred in 2020.