When the pandemic first hit African economies in 2020, executives across the continent knew that banking would never be the same again.

While bankers scrambled to plead with regulators and reassure shareholders, some believed that Covid-19 could fast track the slow movement of African banks to go digital.

“It can be an opportunity for the continent and create new business models,” said Ade Ayeyemi, CEO of Ecobank, one of Africa’s largest banks.

As banks released their yearly results in March, the prediction seems to have held true.

Financial institutions saw large scale customer acquisitions and migration to digital channels.

As a result, Africa’s banks were less severely impacted in 2020 than expected (though the outlook remains negative amid falling profits and a decline in headline earnings).

A key factor to warding off the Covid-19 fallout was whether banks managed to implement a move to digital banking.

Nigerian banks remain resilient

Overall, Nigerian banks saw impressive growth on digital banking platforms and posted better results than their continental counterparts (though they set aside less money for non-performing loans (NPLs)).

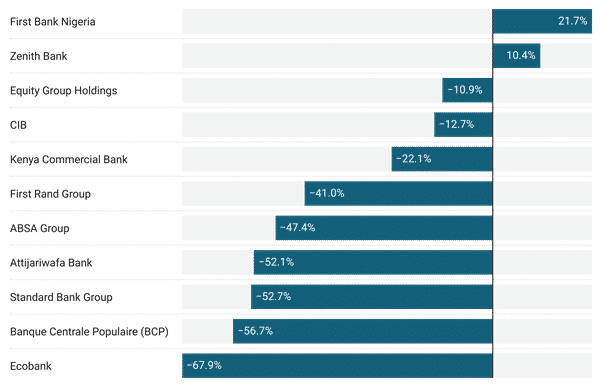

First Bank Nigeria and Zenith Bank, the two biggest banks in Nigeria, posted double digit profit increases while most other African banks were in the red.

The success was supported by an increased spend on digital by Zenith Bank and a strong mobile banking history by First Bank Nigeria.

Zenith Bank, Nigeria’s largest bank by assets, spent $52.5m on IT in 2020, more than double the $23.6m spent in 2019.

While the year-on-year expenditure on travel on hotels plummeted in 2020, IT accounted for around 15.5% of total operating expenses.

Along with increasing profits, the bank managed to grow its loan book by 18% and boosted customer deposits by 15.3%.

United Bank for Africa (UBA), Nigeria’s second-largest bank, recorded a 14.14% increase in its 2020 e-business revenue compared to $102m the year before.

The success has driven the tier-1 bank to capitalise on the shift to digital by releasing a new mobile banking app, which improves the ease of transactions for customers.

Access Bank, Nigeria’s largest bank by total assets, beat all other competitors in the local market to earn $147.4m in e-business revenue last year.

This figure represented a whopping 55.64% increase from 2019, which helped grow overall profit after tax in 2020 by 10.4% to $606m.

The success is no surprise as Access Bank almost doubled the spend on its digital business to $49m in 2020, up from $25m in 2019.

This shows that betting on a digital-first future pays clear dividends; something which is all the more important during a tough operating environment.

However, despite impressive gains in some banks the banking industry in Nigeria reported a 0.24% dip in income from digital channels to $569m in 2020.

The lenders face ongoing subdued growth on the back of an economy that continues to falter despite a slight recovery in oil prices.

In this context, executives must double down on digital revenue streams as an alternative and viable source of income.

This is especially important as well-capitalised digital-only “challenger banks” like Kuda are shaking up the Nigerian market as they attempt to sway customers away from brick-and-mortar institutions by the promise of zero fees.

South Africa suffered

South African banks were some of the worst performers over the pandemic, constrained by a sluggish economy on the back of slow reforms and one of the world’s strictest lockdowns.

Headline earnings were down and return on equity (ROE) for many of South Africa’s banks almost halved in 2020.

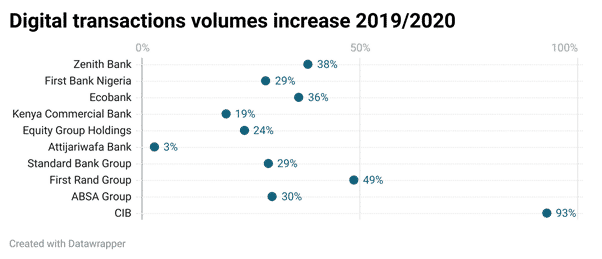

Standard Bank saw headline earnings drop 72% to $1.01bn though the lender was cushioned by operations outside its home market and impressive growth on digital platforms.

Africa’s largest bank by capital and assets saw branch activity in South Africa fall by 44% but mobile activity in the Africa region almost double and online banking grow by 42%.

Turnover from mobile engagement in South Africa grew by 23%, signalling a key area for the bank to invest in going forward.

First Rand Bank reported a 20% decline in normalised earnings due to provisions made for bad debt but posted the second-highest increase in digital traffic behind Egypt’s Commercial International Bank (CIB).

Compared with the six months to end June 2020, Africa’s third-largest bank by assets said there are indications of a positive rebound and digital will be a key part of that comeback.

Full-year earnings from Absa, Africa’s second-largest bank, tell a similar story.

The financial services group reported a 51% decline in headline earnings due to a 163% increase in credit impairments over the Covid-19 period.

While earnings from regional operations across Africa were also down 56%, the number of digitally active customers increased by 23%.

Indeed, the migration of thousands of customers onto digital channels during the pandemic will have provided a key source of revenue while other streams dried up.

Mckinsey argues that African banks should focus on three imperatives to “build core strength and resilience”: productivity, risk management and scaling up the technology.

The consultancy estimates that Africa’s banking industry could lose more than $48bn in cumulative post risk revenue by 2024 if banks fail to adapt to the Covid-19 marketplace.

South African and Kenyan banks may see improved results this year after increasing loan-loss provisions by more than 200% to cover bad debt.

Morocco and Nigeria should set aside more capital, as their current loan-loss provisions might not adequately cover NPLs that loom large on the horizon, Mckinsey says.

East Africa in the middle

Strict lockdowns in most East African countries hit banks throughout the region, though timely interventions by regulators helped the lenders avoid further losses.

Kenyan banks, which are the largest in East Africa, faced a similar but less severe drop in earnings to counterparts across Africa, driven by increased provisions for loan losses and rising NPLs.

KCB, Kenya’s top lender by assets, reported a drop in net profit of 22% while NPLs rose by almost 5%.

During the financial year, the lender doubled down on its digital business by unveiling a mobile app Vooma.

KCB describes it as a “robust, exciting and dynamic new mobile wallet that enables customers to pay for goods and services, get loans and save money through their phone on any network.”

The bank has seen a 66% decrease in the number of branch transactions over the past five years and a 50% reduction in the number of transactions that are processed by branch tellers.

Despite the increase in digital channels, KCB saw a 22% decline in mobile banking revenues due to fee waivers.

Banks must monetize the shift to digital

This speaks to the wider industry issue of how to effectively monetize the shift to digital.

Though millions of customers are now online this does not necessarily mean that revenue will be increased.

Many banks saw customers lead the shift to digital in virtue of lockdowns rather than a perusal of strategy, meaning that some were unprepared to capitalise on the situation.

The digitisation was seen largely only in payments, leaving other segments of operations which are yet to be modernised.

While it is clear that digital-first is imperative, banks will need to decide the best approach to truly build a digital engagement system that puts clients and customers at the centre.

Still, at a time when COVID-19 has put markets across Africa into lockdown and gutted pre-pandemic growth predictions, the fact that banks can continue to transact on digital channels has spared the industry from what would have been a much worse financial year in 2020.

- Cornel Dixon, head of Africa at Backbase