US markets tumbled on Wednesday as investor anxiety spiked over the nation’s growing budget deficit. The Dow lost 1.9%, while the S&P 500 slid 1.6%, marking a broad retreat across major indices.

President Trump’s push to pass a substantial new budget bill by the weekend added to the pressure, with concerns mounting that the fiscal plan could significantly widen the deficit. The sharp move lower served as a stark reminder of how quickly sentiment can shift when financial risks return to the spotlight.

Asian markets slip across the board

Asian Pacific stock indices ended Thursday’s session broadly lower, dragged down by the steep losses seen on Wall Street the day before. The risk-off tone rippled through the region as concerns over the US economy and mounting debt pressures weighed heavily on sentiment.

Investors were also rattled by a sharp drop across longer-dated Japanese government bonds (JGBs), with yield on twenty-year JGBs hitting their highest levels since 2020.

Markets failed to find any meaningful traction overnight, with losses seen across all major indices. Traders remained cautious, mirroring the renewed fears about the global financial outlook and the political uncertainty surrounding the US budget negotiations.

European markets soft at the open

European stock indices were weaker across the board this morning as they tracked the global downtrend. While the downside move was sharp, it appears relatively contained for now.

Yet sentiment remains fragile as investors digest the implications of Moody’s US downgrade last Friday. This morning’s release of Flash Services and Manufacturing PMIs were mostly in line, although there was a notable miss in Germany’s Services update.

Traders are also eyeing any fresh headlines from Washington and elsewhere that could further shape the day’s direction.

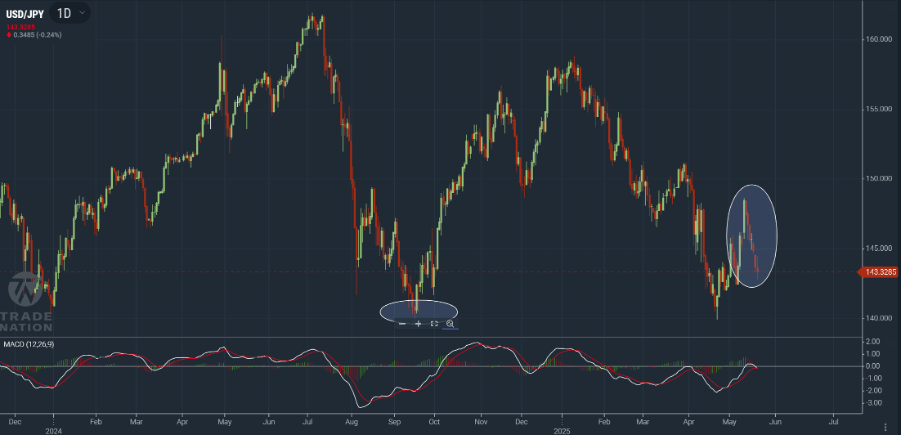

Yen leads as dollar drifts lower

In FX, price action remained relatively subdued. The US dollar continued to soften overnight before recovering a touch as the European session progressed. The Dollar Index hovered above 99.00, having broken below 100.00 at the beginning of the week.

The Japanese yen emerged as the strongest performer overnight, lifted by a return to risk-off sentiment. The USD/JPY has fallen sharply over the last ten days, although it is still somewhere above the lows hit late last summer as the yen carry-trade unwound.

Source: TN Trader

While the dollar’s recent slide has been sharp, traders appear to be waiting for fresh data to dictate the next move. For now, some consolidation could be on the cards.

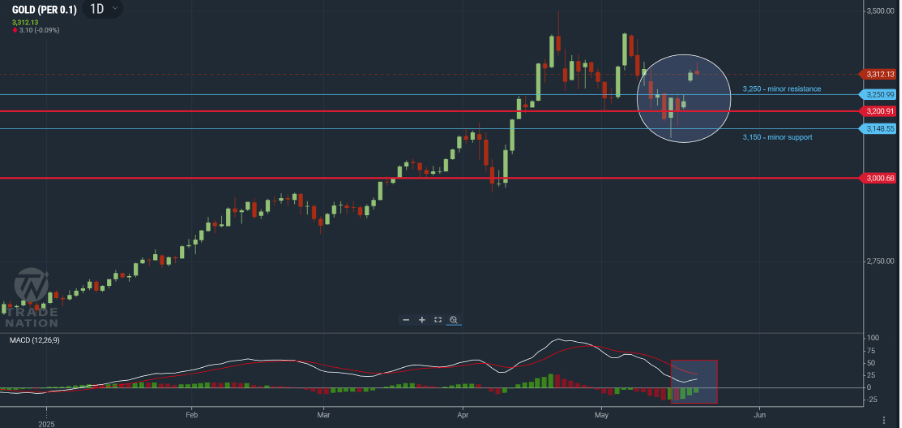

Gold climbs as safe-haven demand returns

Gold pushed higher once again overnight, driven by investor demand for safety amid renewed fiscal concerns. But it gave back all its gains early in the European session. Gold has seen wide intraday ranges in recent sessions, highlighting the volatility in sentiment and positioning.

Source: TN Trader

With debt worries back in focus and equity markets under pressure, gold continues to draw buyers seeking shelter from the storm. But with bond yields ticking higher, it is Bitcoin which is back in favour as the ‘go to’ financial asset.

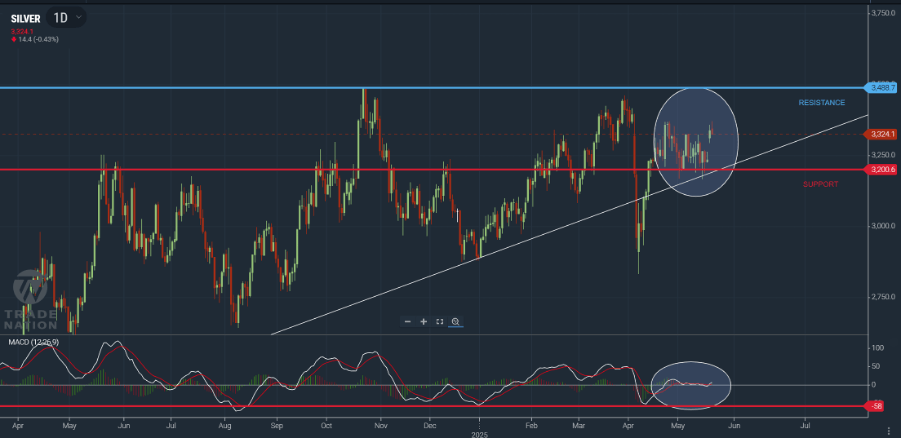

Silver gains, tracks risk mood

Silver also posted modest gains, but like gold, it gave these back early in the European session. It broke through resistance at $33 per ounce on Tuesday, and this level held as support on a pullback yesterday.

The overall tone remains cautious, but sentiment should improve if silver can hold and build above $33.

Source: TN Trader

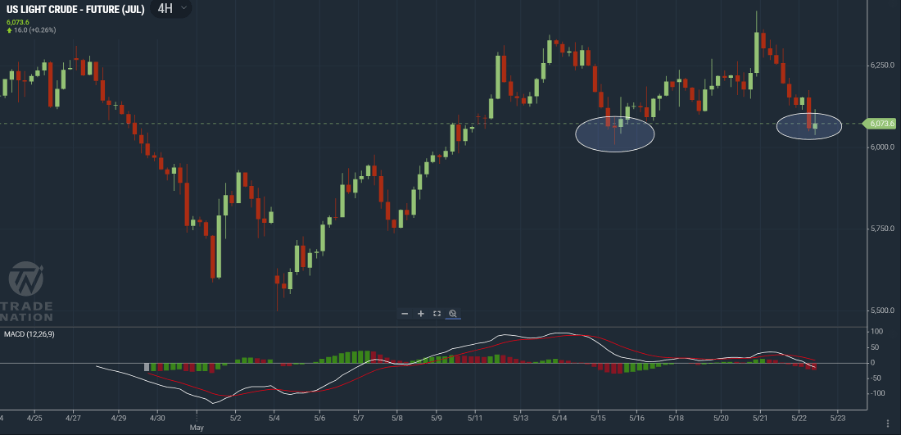

Oil retreats below $61 as supply concerns mount

Oil prices slid overnight, with front-month WTI falling below $61. The decline followed a surprise US inventory build reported on Wednesday, adding pressure to an already fragile demand picture.

With supply increasing and geopolitical developments weighing on sentiment, the momentum has shifted firmly in favour of the bears – at least for now.

Source: TN Trader

Gas flat but testing key levels

Natural Gas ended little changed yesterday, but well off their highs for the session. It has continued to weaken this morning as profit taking continues following Tuesday’s sharp rally.

Bitcoin hits new record above 110K

Bitcoin surged to a fresh all-time high north of $110,000 as the crypto market capitalised on dislocations across traditional financial assets. The move reinforces the narrative of Bitcoin as an alternative investment vehicle, especially during periods of volatility and fiscal uncertainty.

Sentiment remains broadly positive as the digital asset trades in uncharted territory.

VIX edges toward 21 as volatility lingers

The VIX, now trading on the June contract, climbed sharply on the back of the US equity sell-off. Now just below 21, the index reflects the market’s rising concerns around US economic stability and fiscal responsibility. While not at crisis levels, the move signals an uptick in short-term worries as investors reassess their exposure to market risk.

Macro focus: PMI, IFO, jobs and housing

The economic calendar is busy today. Key releases include:

- Manufacturing and Services PMI numbers

- German IFO survey

- US weekly jobless claims

- Housing data

Each data point may offer additional clarity on growth prospects and influence rate expectations moving forward. Markets remain sensitive to any unexpected updates.

Earnings watch: Ralph Lauren before the bell

Fashion house Ralph Lauren is set to report earnings before the open. As consumer discretionary stocks come under increased scrutiny, the report will offer further insight into retail resilience and shifting spending trends in the current macro environment.

Meanwhile, NIKE is set to return to Amazon for direct sales — a notable shift after several years away.

Yesterday, Target shares came under pressure after the retailer posted weaker-than-expected first-quarter results and issued a downbeat forecast for the year ahead. Total revenue fell 2.8% year-over-year to $23.85 billion, missing Wall Street’s estimate of $24.23 billion.

Comparable sales dropped 3.8%, led by a 5.7% decline in in-store activity, partially offset by a 4.7% rise in digital sales.

Looking ahead, Target now expects a low-single-digit decline in full-year sales for 2025, reversing previous guidance that had called for roughly 1% growth.

The company also cut its adjusted earnings per share forecast to a range of $7 to $9, down from a prior view of $8.80 to $9.80 and below analyst consensus. The update underscores ongoing challenges in the retail sector as consumer spending remains uneven.

Geopolitics: Tariff tensions, Putin and Trump talks

Global headlines continue to flow. Reports suggest that Russia’s struggling wartime economy may be pushing President Putin toward renewed peace talks. President Trump’s meeting with South Africa’s leader was described as tense, adding another layer to a crowded geopolitical agenda.

Tariff tensions between the US and China remain front and centre, with Washington’s latest moves aimed at reshaping global manufacturing and trade flows. The pressure has intensified this week, following widespread relief a fortnight ago after both sides slashed their respective tariffs for a period of 90 days.

Meanwhile, inconclusive ceasefire discussions between Russia and Ukraine continue, brokered in part by Trump’s direct engagement with Putin. Thus far, little meaningful progress has been made, and scepticism is mounting over the US’s ability—or willingness—to secure a lasting resolution.

Diplomatic efforts persist on multiple fronts, with European allies still engaged and the Vatican now floated as a potential neutral party to help anchor the peace talks in something more substantive.

Market outlook

Wednesday’s sharp reversal served as a wake-up call for equity bulls. The US budget remains a growing concern, and with the vote looming, market participants are bracing for potential fallout.

Gold’s resurgence and Bitcoin’s new record both highlight the search for alternatives amid mounting uncertainty. With key economic data on deck, the tone could shift quickly again – and volatility, as measured by the VIX, remains very much alive.

- David Morrison is a Senior Market Analyst at Trade Nation

- This article was originally published by Trade Nation. It is republished by TechFinancials under a Creative Commons Attribution-NoDerivatives 4.0 International Licence. Read the original article